Cuando llegue el momento de presentar sus impuestos, deberá decidir si desea realizar la deducción estándar o detallar sus impuestos. Detallar es beneficioso si tiene múltiples inversiones, dona artículos tangibles de alto valor a organizaciones benéficas o tiene facturas médicas elevadas. Sin embargo, con la eliminación de la exención personal, muchas personas consideran que la deducción fiscal estándar es la mejor opción. ¿No estás seguro de cuál es mejor para ti? Consulte los montos de deducción estándar para 2021 y 2022 a continuación, así como nuestros consejos para elegir qué opción tomar.

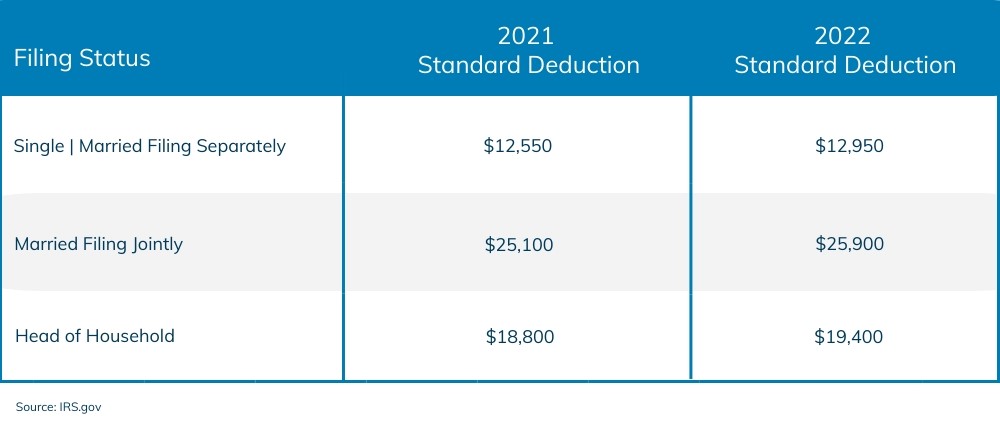

La deducción estándar de 2021 y 2022

El monto de deducción estándar que recibirá se basa no solo en su estado civil para efectos de la declaración, sino también en su edad y otros factores. Los cuadros a continuación incluyen los montos para la temporada de impuestos de este año, así como la temporada de impuestos de 2022 (para las declaraciones presentadas en 2023).

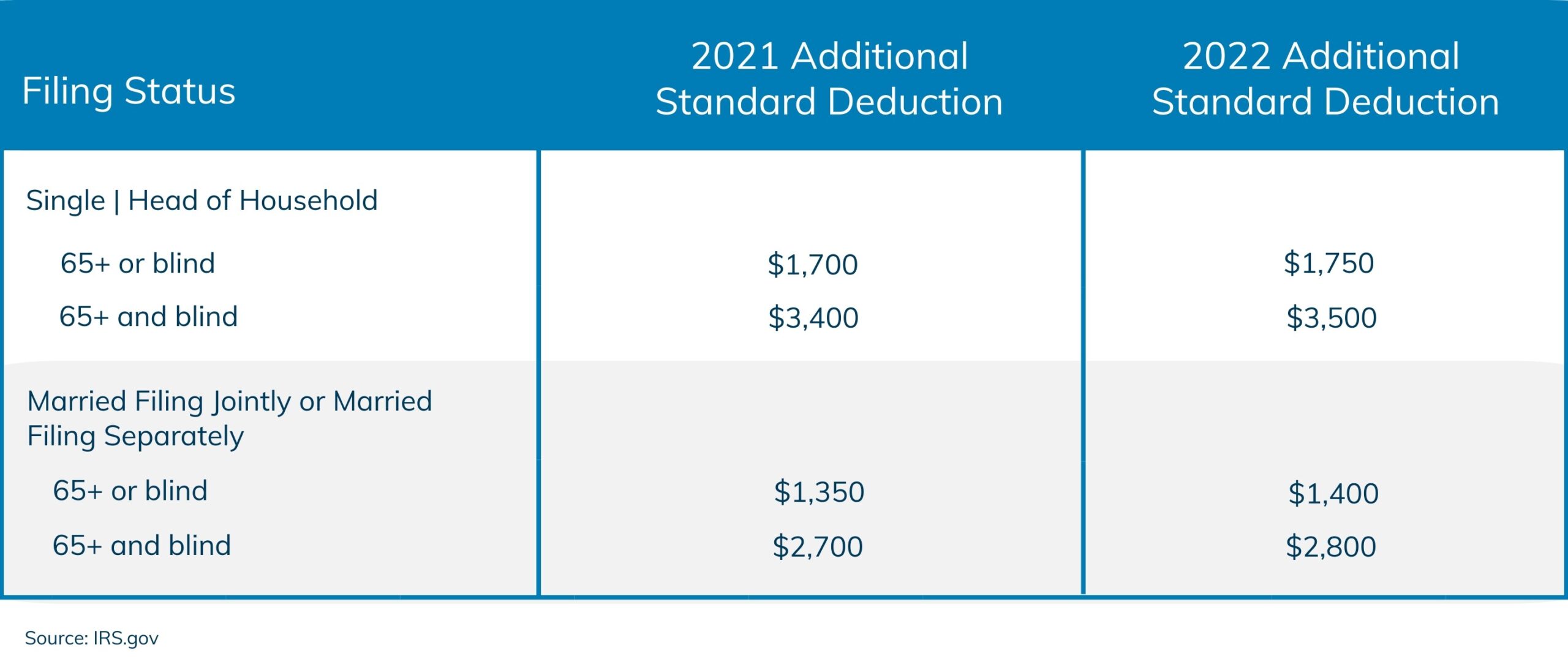

Si tiene 65 años o más, o es ciego, puede reclamar un monto adicional además de la deducción estándar por su estado civil para efectos de la declaración. Según el IRS, se considera que una persona cumple 65 años el día antes de su cumpleaños. Para recibir el monto de la deducción adicional por ceguera, debe estar legalmente ciego al final del año fiscal o pedirle a su oftalmólogo (oftalmólogo u optometrista) que le proporcione una declaración certificada de que no puede ver más de 20/200 en su mejor ojo. con anteojos o lentes de contacto, o su campo de visión es de 20 grados o menos. Asegúrese de guardar una copia de esta carta para sus registros.

A continuación se detallan los montos que recibirá, según su estado civil para efectos de la declaración, si tiene más de 65 años y/o es ciego.

Al presentar una declaración conjunta, tenga en cuenta que el monto adicional se otorga por cada cónyuge que califique.

Deducción fiscal estándar para dependientes que presentan una declaración

La deducción de impuestos estándar puede volverse un poco más complicada si lo declaran como dependiente en la declaración de otro contribuyente. Para la temporada de impuestos de 2021, la deducción estándar es $1,100 o su ingreso del trabajo más $350, lo que sea mayor. Sin embargo, el monto total de la deducción no puede exceder la deducción estándar regular para su estado civil para efectos de la declaración.

A continuación se muestra un ejemplo de cómo funciona esto. Cody es estudiante de segundo año en la universidad y ganó $16,000 gracias a una lucrativa pasantía en 2021. Dado que sus padres lo consideran dependiente en sus impuestos, deberá utilizar uno de los siguientes para su deducción.

- $1,100

- $16,350 (su ingreso del trabajo más $350)

- $12,550

¿Sabes qué cantidad debe tomar? La respuesta es C. Aunque $16,350 es mayor que $1,100, también excede la deducción estándar regular de $12,550 para contribuyentes solteros. Por lo tanto, Cody debe utilizar $12,550 al presentar la solicitud.

Cuándo reclamar la deducción estándar

La mayoría de los contribuyentes utilizan la deducción estándar al presentar sus impuestos. No es necesario guardar recibos y los cálculos son mucho más fáciles de calcular. El monto de la deducción también es mucho mayor gracias a la Ley de Empleos y Reducción de Impuestos (TCJA) de 2017, que casi duplicó el monto para todos los estados civiles.

La principal ventaja de la deducción estándar es que cualquiera puede reclamarla a menos que se encuentre en uno de los siguientes escenarios:

- Está casado y presenta una declaración por separado y su cónyuge detalla las deducciones

- Está presentando su declaración como patrimonio, fideicomiso o sociedad

- Durante el año fiscal, usted era un extranjero no residente o un extranjero con doble estatus

- Debido a un cambio en su período contable, presentará su declaración por menos de 12 meses

En general, querrá tomar la deducción estándar si no posee bienes inmuebles o inversiones, o si no tiene facturas médicas importantes. Sin embargo, no es mala idea preparar sus impuestos utilizando ambos métodos para ver cuál le brinda el mejor resultado.

Cuándo detallar sus impuestos

Aunque la deducción estándar es la forma más fácil de reducir su ingreso imponible al presentar la declaración, no es necesariamente la mejor opción para todos. Por lo general, detallar sus deducciones tiene sentido si usted:

- Tiene gastos médicos no reembolsados (que exceden 7.5% de su ingreso bruto ajustado (AGI)

- Hacer donaciones caritativas (efectivo y artículos tangibles)

- Tener pérdidas por hecho fortuito y robo.

- Pagar impuestos estatales y locales

- Tiene pérdidas de juego

- Poseer un hogar con una hipoteca

Si el total de estas deducciones excede el monto de la deducción estándar, definitivamente vale la pena el tiempo y el esfuerzo. Solo recuerde que deberá realizar un seguimiento de sus gastos y conservar los recibos cuando utilice este método. También recomendamos conservar sus registros durante siete (7) años, en caso de que sea auditado.